Life Insurance Internal Changes and Their Impact on Policy Owners

What’s Happening

Recently the insurance industry has begun to see the fallout of a number of factors from the near past. The combination of a low interest rate environment and general economic turmoil over the past 15 years has led several major insurance companies to raise the internal cost on (non-guaranteed) interest sensitive universal life significantly.

Internal Charges

Life insurance policies contain ‘internal charges’, which include items like the cost of insurance and administration fees. The charges have a current basis and guaranteed basis. In other words, the insurance company cannot contractually charge more than the guaranteed basis, but they usually have room to increase the charges beyond the current basis. A company typically will lower interest crediting rates before changing internal charges if they are not profitable. Increasing internal charges can be much more significant than a crediting rate drop in impacting policy values such as cash value or lapse age and has rarely happened in the life insurance industry historically.

Recent Events

Recently, Banner, Lincoln Benefit, VOYA (formerly ING), AXA and Transamerica are some of the major life insurance carriers that have made internal cost modifications. It is important to note this may not impact all policies issued by these companies and also depends on the specific year of issue and product series of the policy. We expect to see further consolidation in the industry and internal charge increases by additional carriers in the near future due to the economic environment.

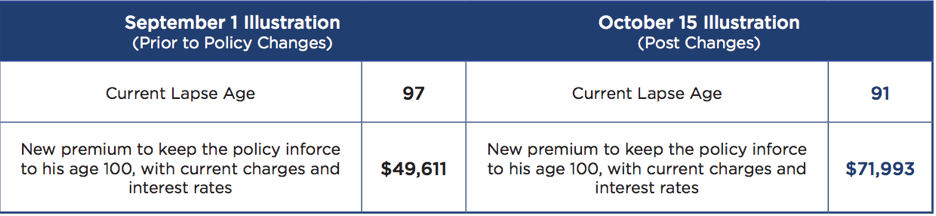

What Does This Mean for My Clients?

Policy Owner: Male, purchased a non-guaranteed (interest sensitive) universal life policy in 2003 at his age 75.

Goal: $1M in death benefit, premium of $40,346 per year, policy to lapse at client’s age 100 (assuming current charges and current crediting rate).

Proformex™ triggered a request for a policy illustration on September 1st and another on October 15th after internal policy charges had been modified.

What Now?

Any client that has a non-guaranteed universal life product or a product from one of the carriers above should review a current inforce illustration, especially if those clients intend to keep the coverage and/or the client(s) is over age 70. No matter the age or timeframe of the client, the longer the situation is ignored, the more expensive and difficult it will be to address the effects of these changes.